Courtesy of iii.org

The official Atlantic hurricane season runs from June through November, but occasionally storms form outside those months. September is the most common month for hurricanes making landfall in the U.S., followed by August and October, according to an analysis of 1851 to 2015 data by the National Oceanic and Atmospheric Administration. No hurricanes made U.S. landfall before June and after November during the period studied.

2018 Hurricane Forecast: Dr. Philip Klotzbach and Michael Bell of Colorado State University (CSU) released an updated forecast for the 2018 Atlantic hurricane season at the end of May. The CSU team now envisions a near-average season with 14 named storms, six hurricanes, and two major hurricanes. The May forecast is slightly lower than their original outlook which called for 14 named storms, seven hurricanes, and three major hurricanes. A typical year has 12 named storms, six hurricanes, and three major hurricanes, according to the National Oceanic and Atmospheric Administration (NOAA). Major hurricanes (Category 3 or higher) have sustained wind speeds of at least 111 miles per hour.

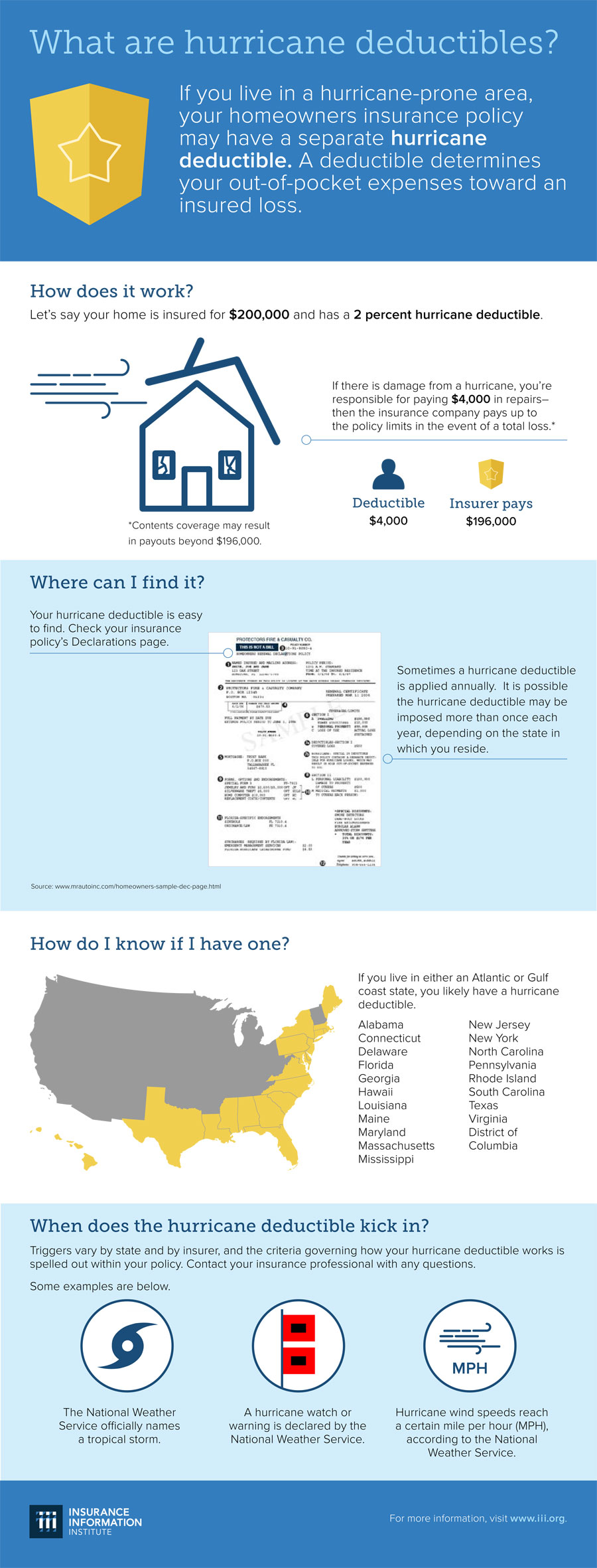

What is a Hurricane Deductible?